2013 Economic Outlook & Calgary Regional Housing Market Forecast

This week the Calgary Real Estate Board released their 2013 forecast. They start with the Global economy and work it down to Calgary. I have tried to summarize the report showing what I think are the highlights. All info is taken from the Calgary Real Estate Boards annual forecast. If you would like a full copy of the report please contact me.

Global Economy: Many of the global economic risks that weighed on the economy through 2012 remain, creating uncertainty and impeding economic growth in to 2013. However while the economy remains fragile, policymakers have options that could help support global finances. If the Euro zone can survive it’s fiscal problems and the US can avoid the political drama in dealing with spending cuts, taxes and the debt ceiling the global economy should grow, albeit slowly.

Europe: This year, economists estimate the European Community will see extremely modest growth, if any at all.

Emerging-market economies: Emerging market growth is slowing in part as a result of policy actions aimed at easing inflationary pressures, along with weaker demand from advanced economies. GDP growth in emerging markets has dropped from 7% in 2010 to an estimated 5.3% in 2012.

United States: The US is growing at a gradual pace with improvements in the labour market and signs of recovery in the housing market. This year the US Economy is expected to gain momentum, if politicians can agree to a long term plan addressing government spending, tax policy and the debt ceiling.

Canada: Global Economic concerns and weak growth are restraining Canadian economic activity this year. National growth is expected to remain at 2% this year; this varies significantly from region to region. Resource rich provinces are expected to lead the country.

Alberta: Alberta’s GDP growth slowed to 3.4% last year but remains one of the leaders in the country’s economic growth. Alberta’s growth is expected to ease to 3% in 2013 and gain momentum in 2014 as the global economic growth finds solid footing.

Calgary: While the pace of growth eased in 2012, Gross Domestic Product for 2012 and 2013 if forecast to grow by 3.3% annually.

Calgary Employment: Improving economic conditions resulted in a growth of 3.4% in 2012 with a surge of full time employment. Employment growth is expected to ease this year to 2.5%.

Calgary Migration: More than 19,000 people migrated to the city in 2012. The rise in migration is the result of stronger job growth here compared to the rest of the country. Net migration levels in Calgary are expected to slow to just more than 15,000 over the next two years.

Calgary Housing Rental: The surge in Migrants to the city fueled increased demand for rental accommodation. Vacancy rates are expected to remain low at 1.5% this year.

Calgary Housing-New Home: New home starts surged in 2012 with 12,400 new starts. This year the forecast is to decline to 11,900 housing starts. The decline is anticipated as multifamily builders reduce production in response to a higher number of units under construction.

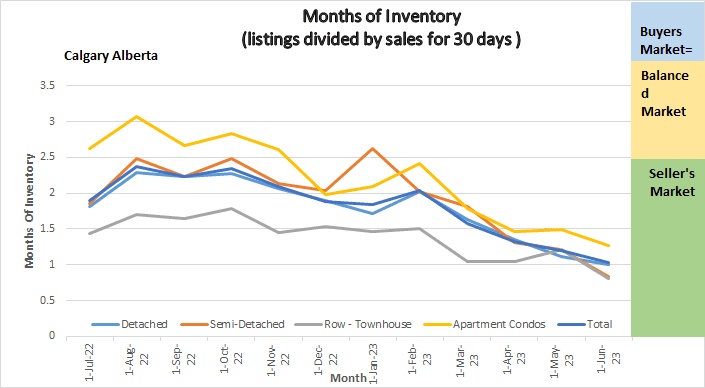

Calgary Housing Resale Market: The resale market gained some momentum in 2012 as sales activity rose both within the city and in surrounding areas. Sales within the city is totaled at 21,207 a 15% increase over 2011. Meanwhile new listings declined by 6.5% causing inventory levels (which have been elevated) to decline by 18% in 2012 from 2011. The decline in inventory put upward pressure on prices. The benchmark prices in Calgary averaged $381,408 in 2012 a 5% rise over 2011.

This year sales growth is expected to ease to 2.2%. Easing growth combined with no significant increase in inventories will keep the resale market in balanced territory. Price growth is expected to be 2.9% this year.

Single Family Home: Prices are estimated to rise by 3% for an annual benchmark price of $437,449.

Condos: Demand for condos is expected to improve as supply in the single family market remains restrained. Condo sales are expected to rise by 3% in 2013. Improved absorption rates should lead to a moderate price appreciation of 2.4% for apartment condos and 2.8% for townhouses.

Surrounding Towns: Sales growth in surrounding towns increased 21% in 2012 helping to reduce the inventory by an average of 13%. Surrounding Towns are expected to outpace Calgary’s growth as surrounding towns enjoy a price advantage over the city.

Forecast Risk – Downside: A significant risk exists in economies if economic conditions worsen in Europe. The other potential risk is our reliance on the US market for energy exports combined with tight pipeline capacity. Weakness in the natural gas market may cause further restructuring and ultimately result in job losses which could harm confidence placing downside risk in the housing sector.

Forecast Risk – Upside:

- If the US is able to resolve internal political uncertainty and its economy expansion accelerates this could be the signal business investors are looking for resulting in higher gains in employment and housing demand.

- If the political unrest in the Middle East increases, leading to disruption in global oil supply, this could drive up oil prices which would benefit Alberta.

- Approval of pipelines could boost confidence in the region increasing demand for housing at greater than expected rates this year.

- If the housing demand outpaces supply this could cause higher than expected price increases especially in single family homes in Calgary.

Forecast Summary: Indicators

|

|

2010

|

2011

|

2012E

|

2013

|

Forecaster

|

|

Calgary GDP Growth (%)

|

3.1

|

3.2

|

3.3

|

3.3

|

Conf board

|

|

Calgary Net Migration

|

-4154

|

9563

|

19658

|

15000

|

City Calgary

|

|

Clag Employment Growth

|

-1.25

|

2.95

|

3.36

|

2.47

|

Conf board

|

|

Mortgage lending rate 5yr

|

4.82

|

4.57

|

4.26

|

4.76

|

Conf board

|

|

Single Family Starts

|

5782

|

5084

|

5700

|

5900

|

CMHC

|

|

Multi Family Starts

|

3480

|

4208

|

6700

|

6000

|

CMHC

|

|

Apt Rental Rates

|

1069

|

1084

|

1150

|

1200

|

CMHC

|

|

Apt Vacancy Rates

|

3.6

|

1.9

|

1.3

|

1.5

|

CMHC

|

|

WTI oil prices (USD)

|

79.4

|

94.86

|

94.26

|

88.38

|

US energy info Admin

|

|

Henry Hub gas spot price

|

4.52

|

4.12

|

2.86

|

3.79

|

US energy info Admin

|

Forecast Summary: MLS Resale Homes City of Calgary

|

|

2010

|

2011

|

2012E

|

2013

|

Forecaster

|

|

Total Sales

|

17,218

|

18,496

|

21,207

|

21,669

|

CREB

|

|

Total New Listings

|

36,994

|

34,068

|

31,847

|

31,528

|

CREB

|

|

Annual Benchmark Price

|

366,258

|

361,758

|

381,408

|

392,469

|

CREB

|

|

Single Family Sales

|

12,043

|

13,120

|

15,109

|

15,381

|

CREB

|

|

SF Benchmark Price

|

400,950

|

418,225

|

424,708

|

437,449

|

CREB

|

|

Condo Apt Sales

|

2933

|

3139

|

3501

|

3613

|

CREB

|

|

Condo Benchmark Price

|

245,917

|

239,817

|

244,992

|

250,872

|

CREB

|

|

Townhouse sales

|

2182

|

2237

|

2597

|

2675

|

CREB

|

|

Townhouse Benchmark Price

|

277,175

|

269,892

|

277,167

|

284,928

|

CREB

|

|

Surrounding town Sales

|

3082

|

3243

|

3970

|

4093

|

CREB

|

|

Surrounding Town Benchmark Price

|

316,333

|

311,708

|

322,450

|

329,544

|

CREB

|